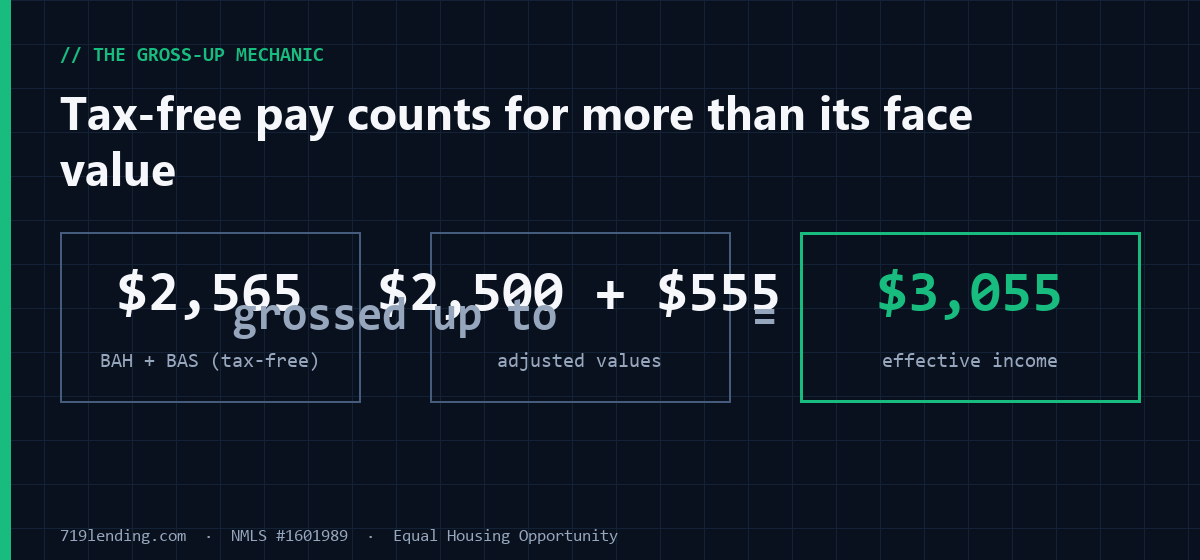

On a VA loan, your military income is more than base pay. BAH and BAS are tax-free allowances a lender can gross up — which quietly raises the income you qualify on. Here's which pay counts, and the charts to prove it.

Understanding VA Loan Eligibility: A Simple Guide for Veterans

Are you eligible for a VA loan? This guide covers the basic requirements, different service statuses, and how to get your Certificate of Eligibility. Find out if you qualify for VA loan eligibility.

Key Takeaways

- VA loans are accessible to eligible veterans and service members, requiring a Certificate of Eligibility to confirm service requirements and allowing borrowers to avoid down payments and mortgage insurance.

- Eligibility for a VA loan varies based on service status, with specific requirements for active-duty members, veterans, and National Guard or Reserve personnel, including potential exceptions for those with unique circumstances.

- The process of obtaining a Certificate of Eligibility can be done online, through a lender, or via a mail-in application, with required documentation varying based on the applicant’s service status.

What is VA Loan Eligibility?

A VA loan is a mortgage backed by the Department of Veterans Affairs (VA) and is available to eligible veterans, active-duty service members, and certain members of the National Guard and Reserves. One of the most significant advantages of a VA loan is that it requires no down payment and does not necessitate mortgage insurance, making it a highly attractive option for those who qualify.

A Certificate of Eligibility (COE) is required for the VA home loan application. Acquiring this certificate is necessary to move forward with your application. This document confirms to lenders that you meet the necessary service requirements for the VA loan benefit. The COE serves as proof of your eligibility, enabling you to continue confidently in the loan process.

However, having a COE alone isn’t enough. Lenders will also review your credit and income to ensure you meet their specific requirements. The COE will also include information on the amount the VA will repay to the lender if you default on the loan, which provides an added layer of security for lenders.

Basic Requirements for VA Loan Eligibility

Meeting specific basic requirements is necessary to qualify for a VA home loan. Generally, eligibility is based on the length of credible active-duty service. For instance, active duty service members must serve a minimum of 90 continuous days to qualify. The VA also considers unique situations that may affect your ability to meet these standard requirements.

Discharge conditions related to hardship or government convenience can enable individuals to qualify for a VA loan even if they do not meet the standard service requirements. This means that even if you haven’t met the typical service duration, you might still be eligible under specific circumstances.

Eligibility Criteria Based on Service Status

Eligibility for a VA loan varies depending on your service status. Whether you’re an active-duty service member, a veteran, or a member of the National Guard or Reserves, the criteria differ slightly. Each category has specific requirements that need to be met to obtain a Certificate of Eligibility.

We’ll explore these criteria according to different service statuses.

Active Duty Service Members

Active-duty service members must have served at least 90 continuous days to qualify for a VA loan. This requirement holds true even during periods of conflict such as the Gulf War. Active-duty members discharged due to specific conditions like hardship or service-connected disabilities may still qualify, even if they haven’t met the 90-day requirement.

The VA provides flexibility for those discharged due to medical issues or other specific conditions, ensuring that individuals who had to leave the service prematurely are not excluded from the benefits they deserve.

Veterans

Veterans’ eligibility for a VA loan depends on the duration and period of their active-duty service. For instance, those who served during World War II, the Korean War, or the Vietnam War have different service length requirements compared to those who served in more recent conflicts.

Minimum service requirement varies depending on the period of service. Understanding these timelines is crucial for veterans to determine their eligibility accurately.

National Guard and Reserve Members

National Guard members qualify for a VA loan guaranty eligibility if they have completed at least 90 days of active-duty service. This active duty must be beyond training and can include times when the National Guard was activated by the federal government.

Reservists must serve at least 90 days of active duty or have six years of creditable service in the Selected Reserve to qualify. These criteria recognize National Guard and Reserve members for their service, granting them access to the same benefits as active-duty counterparts.

Special Circumstances Affecting Eligibility

There are various special circumstances that can affect eligibility for a VA loan. These circumstances ensure that individuals who have served but do not meet the standard requirements can still benefit from VA loans.

We’ll examine these scenarios in more detail.

Discharged Members with Less Than Minimum Service

Certain discharge conditions can make individuals eligible for a VA loan even if they haven’t met the standard service requirements. For instance, veterans discharged due to service-connected disabilities can qualify for a VA loan regardless of their service duration.

Those discharged for hardship or government convenience may also be eligible if they served a minimum period of their enlistment, ensuring veterans who left service prematurely are not excluded from the benefits they deserve.

Surviving Spouses

Surviving spouses of veterans who died on active duty or from a service-connected disability can also qualify for VA loans, provided they have not remarried. To obtain a Certificate of Eligibility (COE), the surviving spouse must provide evidence that the veteran died in service or from a service-related disability.

Required documentation includes military records, the marriage license, and the death certificate, ensuring the surviving spouse can access the benefits earned by their partner.

How to Obtain a Certificate of Eligibility (COE)

The Certificate of Eligibility (COE) proves that you meet the service requirements for a VA home loan, verifying your qualifications to lenders.

There are several ways to request a COE, including online, through a lender, or via a mail-in application using VA Form 26-1880.

Online Application Process

Request a Certificate of Eligibility (COE) online by submitting the application through eBenefits.va.gov. Active-duty service members need a signed statement of service from their commander, adjutant, or personnel officer.

Requesting Through a Lender

Lenders can use the Web LGY system to obtain a COE efficiently, providing a streamlined process for veterans.

Mail-In Application

Request a COE by mail by filling out VA Form 26-1880 and sending it to your regional loan center. Ensure all required information, such as your full name and Social Security number, to avoid delays.

Required Documentation for COE

The COE provides information on the percentage of benefits you are entitled to based on your service history. The documentation required for a COE varies depending on your service status.

Veterans

Veterans must provide their discharge or separation papers (DD214 or equivalent) to apply for a COE. These documents determine eligibility and ensure veterans receive their deserved benefits.

Current Service Members

Active-duty service members must submit a signed statement of military service from their commander or personnel officer, including their name, Social Security number, and date of birth.

National Guard and Reserve Members

Activated national guard member or discharged member must submit their DD214 or equivalent discharge documents to obtain a COE.

Non-activated members need a statement of service signed by a commander.

Common Issues and Solutions in the COE Process

A common issue in obtaining a Certificate of Eligibility (COE) is processing time. It typically takes about 30 days to receive a COE online, but verification might take up to a year in rare cases. Mailing a request usually results in longer processing times compared to online or lender requests.

To expedite the process, ensure all required documents are complete and accurate. If you encounter delays, check the status of your COE request online.

VA Regional Loan Center: Your Resource for VA Loans

The VA Regional Loan Center is a valuable resource for service members, veterans, and their families who are seeking to utilize their VA home loan benefits. The center provides guidance and support throughout the loan process, ensuring that applicants have a smooth and efficient experience. With multiple locations across the United States, the VA Regional Loan Center is easily accessible and committed to helping those who have served in the military achieve their dream of homeownership.

The VA Regional Loan Center offers a range of services, including:

- Assistance with the Certificate of Eligibility (COE) application process

- Guidance on VA loan guaranty eligibility and entitlement

- Support with the loan process, from pre-approval to closing

- Information on VA home loan benefits and requirements

Whether you’re a first-time homebuyer or a seasoned veteran, the VA Regional Loan Center is here to help you navigate the VA loan process and make the most of your benefits.

Service-Connected Disability and VA Loan Eligibility

Service-connected disability can have a significant impact on a veteran’s life, but it doesn’t have to affect their ability to secure a VA home loan. In fact, the VA offers special benefits and considerations for veterans with service-connected disabilities.

To be eligible for a VA home loan, veterans with service-connected disabilities must meet the same basic requirements as all VA loan applicants, including:

- Having a valid Certificate of Eligibility (COE)

- Meeting the minimum service requirement

- Having a satisfactory credit history

- Meeting the VA’s income and employment requirements

However, veterans with service-connected disabilities may be eligible for additional benefits, such as:

- Exemption from the VA funding fee

- Increased loan guaranty entitlement

- Special consideration for loan approval

The VA also offers a range of resources and support for veterans with service-connected disabilities, including:

- The VA’s Vocational Rehabilitation and Employment (VR&E) program

- The VA’s Home Loan Guaranty Service

- The VA’s Disability Compensation program

VA Home Loan Benefits

VA home loans offer a range of benefits for service members, veterans, and their families. Some of the most significant advantages of VA home loans include:

- No down payment requirement: VA loans offer 100% financing, eliminating the need for a down payment.

- Lower interest rates: VA loans often have lower interest rates than conventional loans, saving borrowers money on their monthly mortgage payments.

- No mortgage insurance: VA loans do not require mortgage insurance, which can save borrowers hundreds or even thousands of dollars per year.

- Lenient credit requirements: The VA has more lenient credit requirements than many conventional lenders, making it easier for borrowers to qualify for a loan.

- Lower closing costs: The VA limits the amount of closing costs that can be charged to borrowers, saving them money on upfront fees.

- No prepayment penalty: VA loans do not have prepayment penalties, allowing borrowers to sell their home or refinance their loan without incurring additional fees.

In addition to these benefits, VA home loans also offer a range of other advantages, including:

- Government-backed guaranty: The VA guarantees a portion of the loan, reducing the risk for lenders and making it easier for borrowers to qualify.

- Flexibility: VA loans can be used to purchase a primary residence, a vacation home, or even an investment property.

- Portability: VA loans are portable, meaning that borrowers can take their loan with them if they move to a new home.

Overall, VA home loans offer a range of benefits and advantages that can help service members, veterans, and their families achieve their dream of homeownership.

Next Steps After Obtaining Your COE

After receiving your Certificate of Eligibility, select a lender specializing in VA loans. Get pre-qualified and then pre-approved to understand your budget for home shopping. The property must meet safety and sanitary standards, which may require repairs before approval.

Once you find a home and have a purchase agreement, officially apply for the VA loan. The lender will review your credit and financial situation, and the underwriter will review your loan application before giving a ‘clear to close’ notice.

Closing involves signing all necessary paperwork to finalize the loan and transfer property ownership.

Summary

Understanding VA loan eligibility is crucial for veterans and their families to take full advantage of the benefits available to them. This guide has covered the basic requirements, eligibility criteria based on service status, special circumstances, and the steps to obtain a Certificate of Eligibility.

By knowing the process and preparing the required documentation, you can navigate the VA loan process with confidence. Utilize your hard-earned benefits and take the necessary steps to secure your home loan.

Frequently Asked Questions

What is a VA loan?

A VA loan is a mortgage insured by the Department of Veterans Affairs, provided to eligible veterans, active-duty service members, and specific National Guard and Reserve members. This financing option helps facilitate home ownership for those who have served in the military.

What is a Certificate of Eligibility (COE)?

A Certificate of Eligibility (COE) is a crucial document that verifies your eligibility for a VA home loan, and it is required for the loan application process. Obtaining your COE is the first step in securing your VA benefits for home financing.

How can I obtain a COE?

To obtain a Certificate of Eligibility (COE), you may request it online, through a lender, or by submitting a mail-in application using VA Form 26-1880. Each method provides a streamlined way to access your COE efficiently.

What documents do I need to apply for a COE?

To apply for a Certificate of Eligibility (COE), veterans must provide their DD214 discharge papers, while active-duty members should submit a signed statement of service, and National Guard members require similar service records. Ensure you have the correct documents to facilitate the application process.

What are the next steps after obtaining a COE?

After obtaining a Certificate of Eligibility (COE), the next steps are to select a lender, get pre-qualified and pre-approved for a VA loan, find a home, apply for the loan, and complete the closing process. Following this path will help ensure a smooth home-buying experience.

Related Posts